-

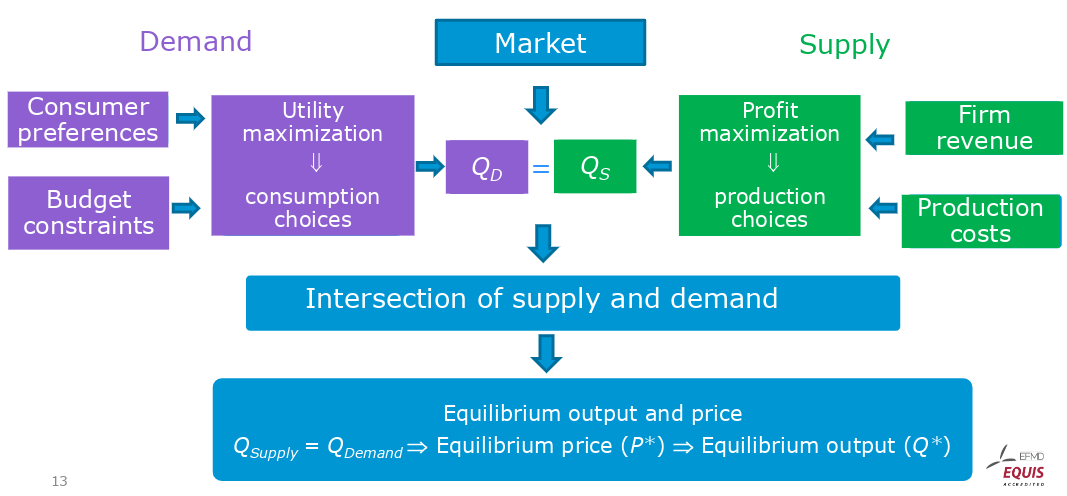

each consumer makes individual choices

-

aggregation of all consumers creates the demand

-

consumer faces value maximization problem

-

each company makes individual choices

-

aggregation of all companies creates the supply

-

company faces profit maximization problem

Supply and Demand require Competition! There cannot be Supply and Demand in a Monopoly.

Supply

- variable

- price of the good

- constants (can change over time)

- technology → Feral Futures, Disruptive Technologies

- prices of inputs

- taxes

Demand

- variable

- price of the good

- constants (can change over time)

- preferences → Customer Perspective

- income → Poverty, Prahalad

- prices of other goods

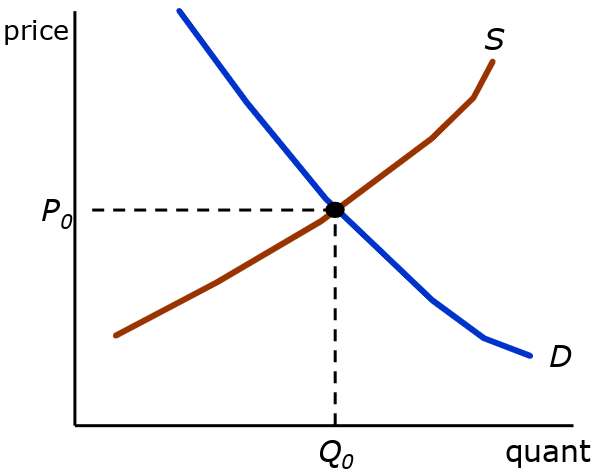

Equilibrium

- intersection of supply and demand function

- Game Theory → no need to act by either consumer or producer

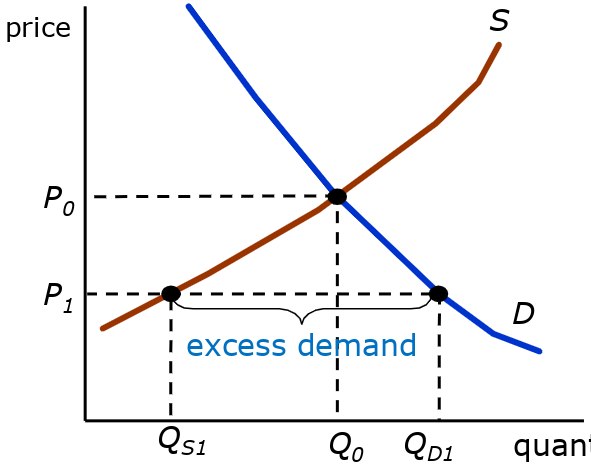

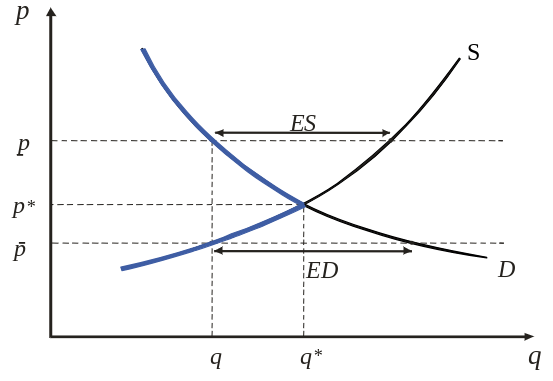

Excess Demand

- consumers demand more than suppliers are willing to supply

- price will increase, supply will increase, demand will decrease

- reaching equilibrium eventually → convergence

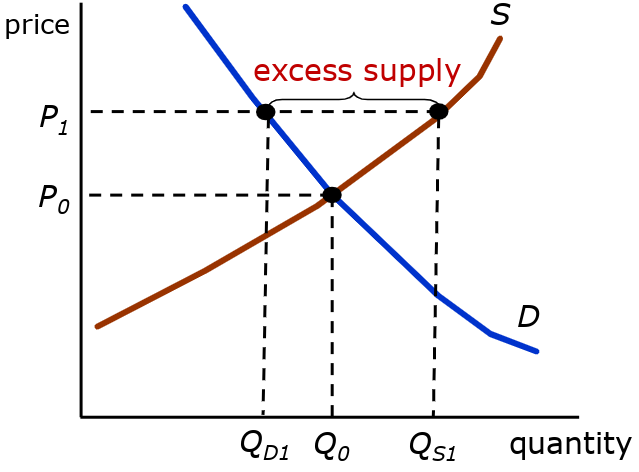

Excess Supply

- consumers demand less than suppliers are willing to supply

- price will decrease, supply will decrease, demand will increase

- reaching equilibrium eventually → convergence

Market Mechanism

- there is only too little supply or too little demand

Shift Equilibrium

- change of supply inversely affects price

- change of demand directly affects price

Price Elasticity

- Marginal Changes

- Elasticity

- Cross-Elasticity

- price elasticity of demand ⇐ 0

- price elasticity of supply >= 0

- “arc elasticity” … taking the average slope along a price range

- used for analyzing the sensitivity of different variables