Identical Products

- compete through price rather than quantities

- oligopolistic industry

- equilibrium price depends on homogeneity of products

- applicable when changes in capacities are easy to make

Bertrand Paradox

- homogenous products

- one firm undercuts the others

- other firms have to adjust (or undercut others themselves)

- strong incentive to undercut everyone

- strong incentive to keep decreasing until p = MC

- just 2 firms are enough to reach equilibrium

- shows importance of strategic variables (price vs quantity)

- is a form of Nash Equilibrium

- criticism:

- seems unnatural for firms (gentlemen’s agreement)

- even at equal prices the firms do not share the market 50/50 necessarily

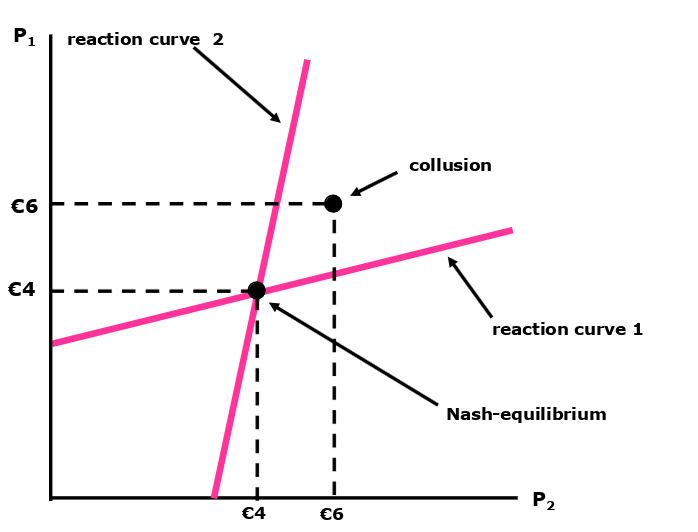

Different Products

- small differences (still same market)

- each firm sets it’s own price and takes price of competition as given

- oligopolistic industry

- profit maximization:

P1∗=2b1a+b2+P2+c1b1

- afterwards same thing for $P_{2}^{*}$

- then solve for both unknowns $P_{1}$ and $P_2$

- result:

- when firm 2 increases prices, firm 1 should increase prices as well

Graphically

- Collusion … Cartel price setting

- related to Dilemma Games

- it would be best (highest profit) for both companies to collude

- but competing is always the dominant strategy