Maths of Correlation

-

covariance

- Covariance

- Covariance and Correlation

- reminder: independent (unrelated) → covariance = 0

- BUT covariance = 0 does not imply independence

- estimation

-

correlation coefficient (Karl Pearson)

- for population:

- for sample:

-

notation

- … sum of squared standard deviations

- is to be minimized in method of least squares

-

equivalent representation

-

correlation is measure of linear relation

-

correlation does not mean causality

-

… between -1 and 1

- sign indicates direction of the correlation

-

shows the strength of the correlation

-

… symmetrical

Proof of

- given

- short form:

- long from: Proof of Correlation Coefficient

- is -1 or 1, depending on sign of

Non-Linear Correlation

- if the data has non-linear correlation (e.g. quadratic, exponential) it is impossible to measure with

- but might be possible with e.g

- a scatter plot is always helpful to understand the problem and choose the correct correlation function

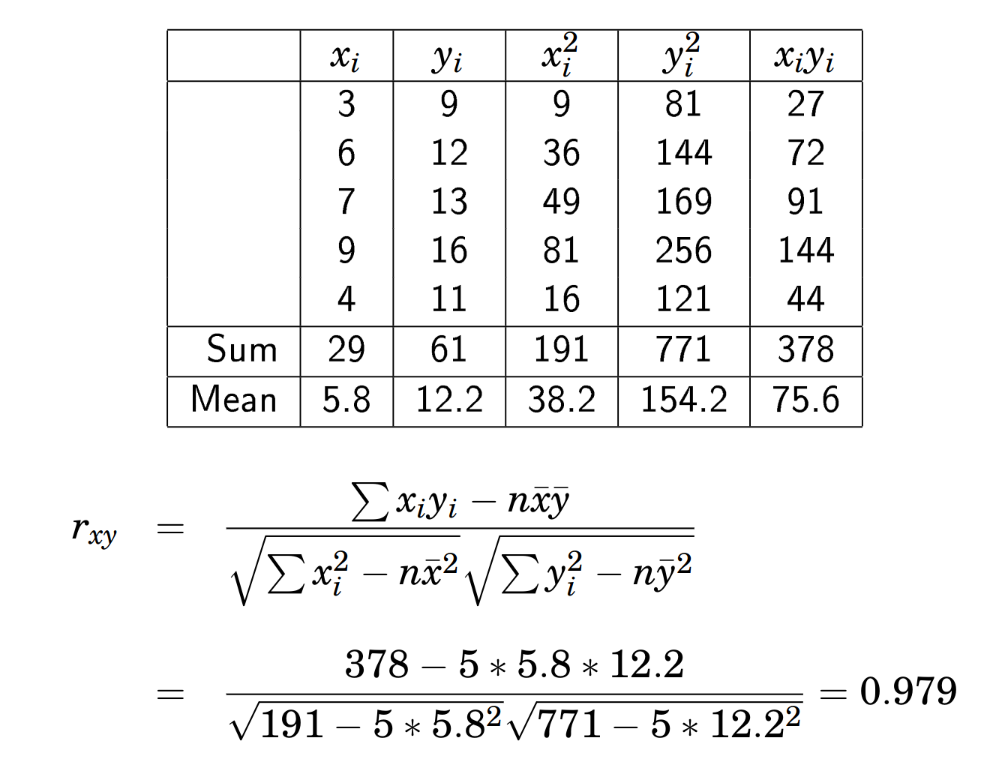

Example Correlation from Table