Scopes

Scope 1

- direct emissions

- directly caused by company by burning of fossil fuels

- e.g. steel production, company cars, combustion generator in the basement

Scope 2

- direct energy consumption

- e.g. electricity consumption, Fernwaerme, cooling, steam

Scope 3

- indirect emissions

- scope 3 cannot be calculated directly

- information has to be given from suppliers

- some suppliers don’t even have that data

Upstream

- purchased goods

- capital goods

- fuel and energy related activities

- waste generated in operations

- business travel

- employee commuting

- upstream leased assets

Downstream

- downstream transportation and distribution

- processing of sold products

- use of sold products

- e.g. company selling diesel generators

- end-of-life treatment of sold products

- important for electric cars

- downstream leased assets

- franchises

- investments

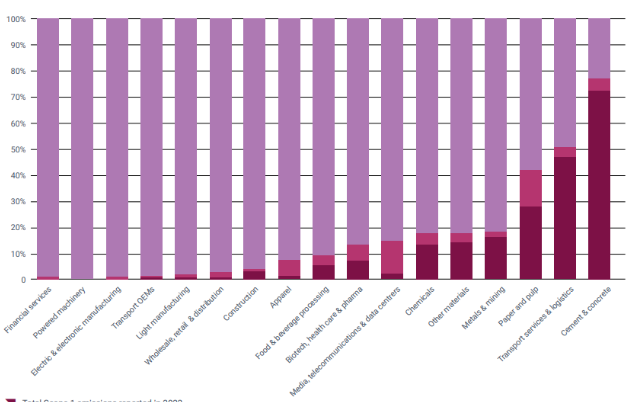

How they are important

- most companies have high Scope 3 emissions

- therefore push to sustainability standards

But there is more than CO2

- reporting only done in CO2eq

- if there are other greenhouse gases (e.g. methane) they are translated into the equivalent CO2 amount

- multiply by global warming potential

- e.g. currently x27 for methane CH4, x273 for nitrous oxide N2O

- they are added up to be just 1 CO2 amount

- possible to have 0 actual CO2 emissions but still report high CO2 emissions which are translated methane