Why is it important?

- climate scientist underestimate recent warming effects

- extreme weather anomalies reaching higher than ever before

- Austria

- average temperature deviation rising

- +2.6 degrees on average, more in cities than in mountains

ESRS

GHG Protocol Standards

- product carbon footprint

- technically hard to calculate

- 2 different perspectives on the same emissions

- e.g. apple, emissions of the whole company vs emissions per iPhone produced

- not double-counting, since it is the same emissions, but different perspective

- one could also argue everything is double counted…

Generally Accepted GHG Accounting Principles

- relevance

- report must reflect the actual emissions

- completeness

- consistency

- consistency over time to allow for easy comparison

- transparency

- data sources

- assumptions

- calculations

- accuracy

- everything is an estimation

- but the goal is to remove uncertainties and not over/underrepresent emissions

GHG Accounting Process Steps

- get data

- decide on boundaries and calculation schemes

- also dependent on data available

- boundaries for organization and for operations

- analyse data and calculate GHG Emissions

- stick to it and report correctly

Setting Organizational Boundaries

- equity share approach

- control approach

- if there is operational control the emissions of the controlled entity are 100% of the controlling entity

Scope 1 Emissions

- identify sources

- stationary/mobile combustion, fugitive emissions, process emissions

- select calculation approach

- direct measurement, stoichiometric calculations, estimates

- collect data and choose emissions factors

- mostly emission data is written on the invoice

- just not integrated yet in the ERP system of most companies

- would allow for integrated calculations

- data levels

- primary: consumption in liters of fuel

- secondary: mileage of car

- tertiary: amount spent on fuel

- apply calculation tool

- convert all emissions to CO2eq

- roll-up data to corporate level

Scope 2 Emissions

- identify sources

- electricity, steam, heat, cooling

- select calculation approach

- market based vs location based approach

- location … geographic location

- market … contracts, purposeful decision

- collect data and choose emissions factors

- metered electricity, utility bills

- consumption in kWh

- emissions per kWh from different energy providers

- apply calculation tools

- convert all emissions into CO2eq

- roll-up data to corporate level

Scope 3 Emissions

- GHG Protocol

- screening

- based on all 15 categories of GHG Protocol

- identify significant categories based on estimated emissions

- calculation

- calculate and estimate as best as possible

- update

- update scope 3 every year

- full inventory (scope 1 and 2 too) only every 3 years

- or when significant change

- not include

- emission offsetting / emission trading → transparency

- reflect actual emissions

Process

- describe the value chain

- data collection and initial assessment

- supplier data

- hybrid data

- average data (secondary process data)

- e.g. aggregate miles of flights booked

- spend-based data (tertiary accounting data)

- e.g. aggregate of cost of flights booked

- materaility and screening → Materiality Assesment

- selection of relevant categories

- selection of calculation methods and calculation

- depends on data available

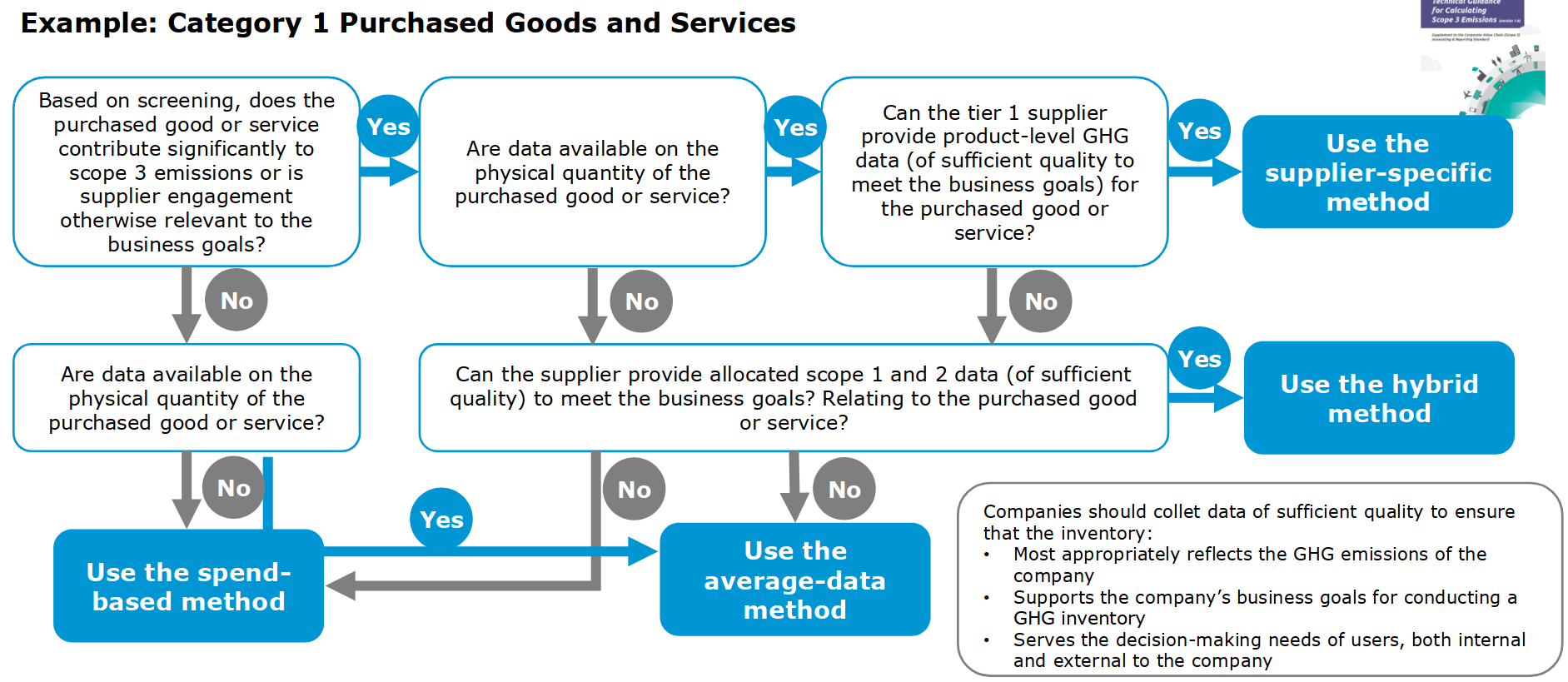

- supplier-specific method

- aggregate of all suppliers

- hybrid method

- aggregate of supplier data you have, extrapolate for the rest

- average data method

- take average of emissions per unit consumed you have, multiply by consumption

- spend-base method

- take average of emissions per expenses you have, multiply by expenses

- results and interpretation

Neutrality vs Net Zero

Climate Transition Plan

- compatibility with paris agreement

- decarbonization levers

- quantification of investments

- climate change mitigation actions

- locked-in GHG Emissions

- e.g. a new plant has been built 5 years ago which is running on gas-generators

- that plant will not be touched in the next 20 years probably

- taxonomy regulation

- plans on reaching higher alignment

- business strategy

SBTi