General

- goal is redirecting capital flows

- targeting banks and other investors when giving out loans

- 2 parts

- does not need to be transposed → regulation

- in effect since 2021

- EU classifies what is green and what isn’t

- addresses Green Washing → less approved

- DWS Case

- activists challenge green washing

- rather report honest 0% alignment than fake 10%

- any kind of defense industry is not deemed as green

- defense industry will hopefully face higher financing costs therefore

- addresses Green Washing → less approved

- have to separately report on

- Revenue

- CAPEX

- OPEX

- generates a percentage on how much money is used or made for/from green endeavors

- problems:

- perspectives change rapidly (e.g. is nuclear energy green or not?)

- laws are slow to change (technological advancements may be too fast)

- problems:

- collecting data on all subsidiaries around the world

- digital infrastructure

- data collection (finding out about data points)

- Digital Tagging

- digital infrastructure

Incentives

- since incentives are only in full (e.g. all of a plant is powered by hydrogen) the incentive if 100% coverage is not possible to just not indulge in it anyways

- a razor blade separating into feasible and non-feasible options, no mix between them possible

Qualitative Reporting Requirements

- accounting method

- how was aligned Revenue/CAPEX/OPEX determined

- double counting

- methodology to avoid double counting

- economic activities

- explanation of relevant activities and weights

- additional information

- relevant background information

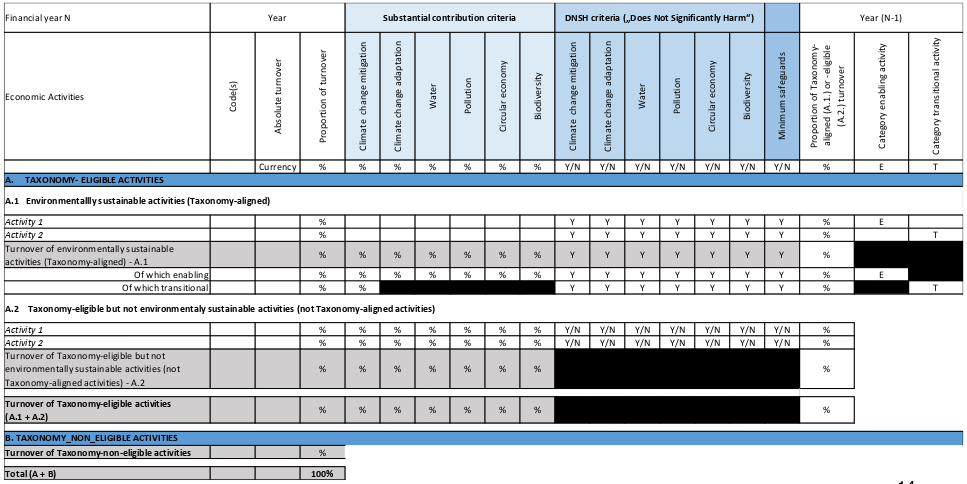

Taxonomy Table

- for each of Revenue, CAPEX, OPEX a separate table

- percentage of aligned/not aligned activities

Legal Stuff

- EU 2020/852

-

- delegated act 2021/2139 (objectives 1-2)

-

- delegated act 2023/2485 (objectives 1-2)

-

- delegated act 2023/2486 (objectives 3-6)

-

- delegated act 2022/1214 (include nuclear and gas energy)

- transitional only

- delegated act 2022/1214 (include nuclear and gas energy)

-

- official tools

- EU Taxonomy Regulation Compass (very helpful)

- EU Taxonomy Calculator

- EU Taxonomy FAQs C/2023/305

Parents/Subsidiaries

- each subsidiary large enough has to report on their own, even if included in parents consolidated report

- subsidiaries not large enough to report on their own can be just included in parent company

Environmental Objectives (art 9)

- climate change mitigation

- climate change adoption → similar to E1 mandatory before 2024

mandatory after 2024 3. sustainable use and protection of water and marine resources → similar to E3 4. transition to a circular economy → similar to E5 5. pollution prevention and control → similar to E2 6. protection and restoration of biodiversity → similar to E4

What to do?

-

Taxonomy Eligibility: screening of economic activities

- if it is listed, it can be aligned

-

substantial contribution

- to one of the objectives

-

do no significant harm

- to other the objectives than the contributed to one

-

minimum safeguards

-

= taxonomy alignment in % for each economic activities

-

then sum up alignments of activities by weight of economic expenditure

-

= total taxonomy alignment in %

- for CAPEX/OPEX/Revenue separately (influences weights)

Shortcomings

- political

- some unsustainable practices deemed as sustainable and vice versa e.g. Germany and gas power generation

- quite technical

- only focus on environment

- very little social or governance aspects

- there are plans to integrate a social aspect as well

- would include: decent work, adequate living standards, inclusive & sustainable societies

- finalization not before 2025, probably later

- there are plans to integrate a social aspect as well

- very little social or governance aspects

- minimal safeguards

- does not prohibit unsustainable activities, only disclosure requirement

- Transparency Theory still applies

- exhaustive list

- economic activities can be missing → All Activities in an Economy - Sustainable View

- e.g. company is reporting 50% not-aligned, 20% aligned, 30% not-eligible

- 30% not eligible can be sustainable, but are not even included, because exhaustive list

Empirical Evidence

wontfix L5 15-18